Picture this. It is October 2024. The Nifty has just slipped 8% from its September peak. Across India, in a single month, over 39 lakh systematic investment plans are quietly cancelled. WhatsApp groups light up with calls to "exit and re-enter," YouTube finfluencers shout "crash is here," and Telegram tip channels promise to "save your capital with options." A few months later, the SEBI study lands: 91% of individual derivatives traders in India lost money in FY25, with a combined loss of ₹1.05 lakh crore.

Now picture another investor. She does nothing in October 2024. Her SIP runs on the 5th of every month, exactly as it has for the last seven years. She has not opened a derivatives account. She has not bought an NFO. She has not even logged into her broker app this week. She has, however, recently finished reading her third investment book of the year.

Five years from now, those two investors will live in completely different financial universes. The difference will not be intelligence. It will not be luck. It will not even be market timing. The difference will be the books they did, or did not, read.

Why Investment Books Matter More Than Ever in India

India is in the middle of a financial-services supercycle the size of which the country has never witnessed before. Demat accounts crossed 21.6 crore by December 2025. Mutual fund assets under management hit an all-time high of ₹81.92 lakh crore by April 2026. Monthly SIP inflows touched a record ₹29,529 crore in October 2025, with more than 9.45 crore contributing SIP accounts. On paper, India looks like a nation of investors.

But scratch the surface and the picture changes. According to the SEBI Investor Survey 2025 (released in January 2026), only about 9.5% of Indian households actually invest in securities — compared to 62% of American adults who own stock. Worse, only 36% of Indian investors are rated as having moderate-to-high product knowledge. The 91% F&O loss rate is not a statistic. It is a national tragedy unfolding one ₹2 lakh-loss trader at a time.

The Hidden Cost of Financial Illiteracy

Between FY22 and FY24, individual F&O traders in India lost over ₹1.8 lakh crore collectively, with the average trader losing roughly ₹2 lakh including transaction costs (SEBI press release, 23 September 2024). The FY25 update worsened these numbers. Behind each of those numbers is a salary slip, a wedding fund, or a child's tuition that no longer exists.

This is where books quietly do their work. A ₹400 book that teaches you to ignore Mr. Market, automate your SIP, and refuse F&O is, in cold rupee terms, the highest-ROI financial product available to any Indian today. SEBI Chairman Tuhin Kanta Pandey, speaking at an investor seminar in November 2025, put it plainly: financial literacy is "the foundation of empowerment, enabling individuals to understand how to save, invest and protect their hard-earned money." Books are still the most patient teachers.

How We Picked These 5 Books

The internet is awash with "best investing books" listicles. Most of them copy-paste the same American classics that have been recycled since 1990. That is not what the Indian investor of 2026 needs. We built our shortlist on five honest criteria:

India relevance. Either the book is written by an Indian for Indian markets, or its principles translate cleanly to NSE, BSE, SIPs, mutual funds and Indian tax structures.

Behavioural depth. The book must address how Indian investors actually think and misbehave — not just what to buy.

Track record. The book has been endorsed by working fund managers, SEBI-Registered Investment Advisers, or has consistently sat on Amazon India's finance bestseller list for years.

Range. The five books together cover mindset, system, strategy, framework and behaviour. Each fills a different layer of an investor's brain.

Value for money. The full reading list costs under ₹2,000 — less than one bad F&O trade.

Now to the books themselves, ranked in the order in which we believe a beginner should read them.

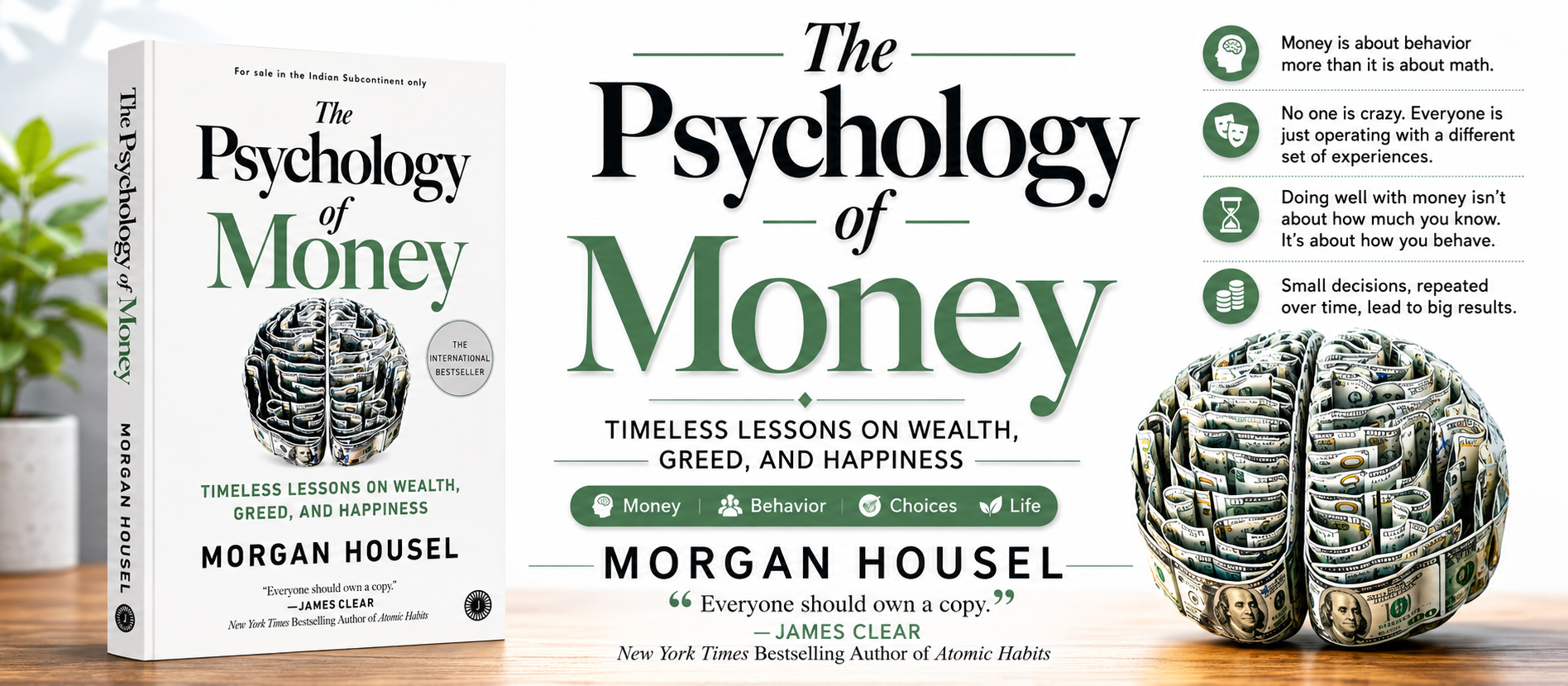

#1. The Psychology of Money — Morgan Housel

The Psychology of Money

Author: Morgan Housel | Published: 2020 | Publisher: Harriman House (Jaico in India)

Pages - 256

Reading Time~6 hours

Price (India) ₹250 – ₹350

Best For - Absolute beginners to advanced

Difficulty - Easy

Languages - English, Hindi, Marathi, Tamil & more

If you only ever read one book on money, make it this one. Housel — a former columnist at The Wall Street Journal and The Motley Fool — opens with a sentence that should hang on every Indian investor's wall:

"Doing well with money has little to do with how smart you are and a lot to do with how you behave. And behaviour is hard to teach, even to really smart people."

This is the single most important insight for an Indian retail investor in 2026. The 91% of F&O traders who lose money are not unintelligent — many are engineers, doctors, and MBAs. Their problem is psychological, not analytical. Housel diagnoses the disease in 19 short, beautifully written essays.

Key Concepts and Frameworks

No one is crazy. Every investor's behaviour reflects their personal money history. Your parents distrust equity because they lived through Harshad Mehta. Your generation chases F&O because you grew up watching Zerodha ads.

Luck and risk are siblings. Treat both Rakesh Jhunjhunwala's success stories and your neighbour's IPO listing with healthy skepticism. You may be looking at survivorship bias.

Compounding is the eighth wonder of the world. A ₹10,000 monthly SIP at a 12% annualised return for 30 years becomes roughly ₹3.5 crore. The catch: you cannot interrupt it.

Getting wealthy versus staying wealthy require opposite skills. Optimism creates wealth; paranoia preserves it. Most Indians know only the first half.

Tails drive everything. A handful of stocks (think HDFC Bank, Asian Paints, Bajaj Finance, Titan over 20 years) generate the bulk of all index returns. The rest are noise.

Reasonable beats rational. A "good enough" plan you can stick to in a crash beats a perfect plan you abandon.

Room for error. Always keep 6–12 months of expenses in a liquid fund before going aggressive in equities.

Famous Quotes

"Wealth is what you don't see."

— Morgan Housel

"The ability to do what you want, when you want, with who you want, for as long as you want, is priceless. It is the highest dividend money pays."

— Morgan Housel

Indian Context Application

This book quietly demolishes the case for active stock-picking by most retail investors. The "tails drive everything" chapter is the strongest argument ever made for buying a Nifty 50 index fund and never looking at it. The chapter on "Reasonable Rather Than Rational" justifies the slightly-imperfect-but-consistent SIP over the perfectly-timed lump sum that never gets invested.

Criticisms

The book is light on technique. There are no stock screens, no valuation formulas, no asset-allocation models. Some essays repeat themes. American examples (Ronald Read, Jesse Livermore, Vanguard) can feel distant. None of this matters. You read this book for the brain rewiring, not the toolkit.

One-line takeaway: Automate your SIP, then do not touch it for ten years.

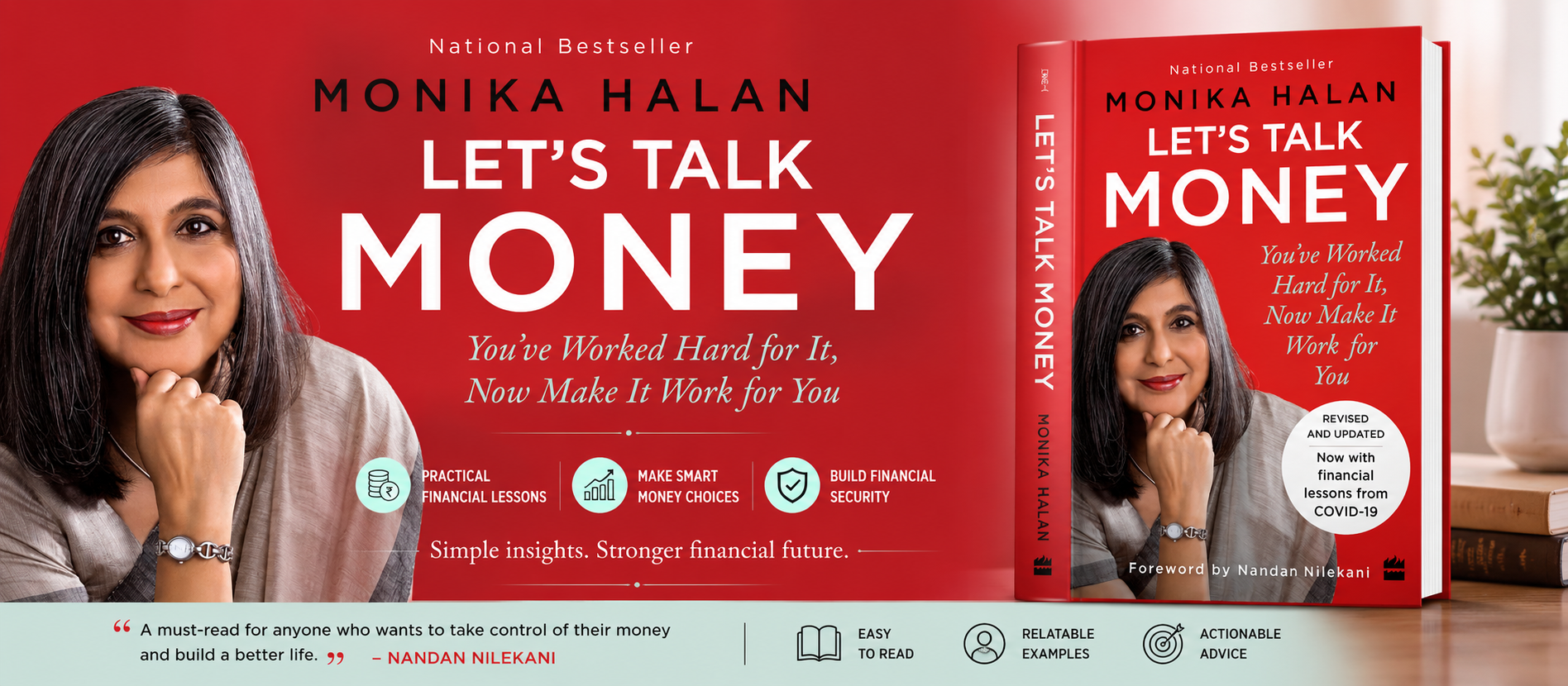

#2. Let's Talk Money — Monika Halan

Let's Talk Money: You've Worked Hard for It, Now Make It Work for You

Author: Monika Halan | Published: 2018 (3rd edition 2024) | Publisher: HarperCollins India

Pages - 204

Reading Time~5 hours

Price (India) - ₹250 – ₹350

Best For - Salaried Indians, first earners

Difficulty - Easy

Languages - English, Hindi (Baat Paise Ki)

Buy on amazon

If The Psychology of Money is the brain, Let's Talk Money is the plumbing. Monika Halan — consulting editor at Mint, a member of SEBI's Mutual Fund Advisory Committee, and arguably India's most trusted personal-finance writer — does not waste a single page. She walks the Indian household, step by step, through the complete personal-finance system most people piece together over a lifetime of expensive mistakes.

This is the book to gift to anyone who has bought a ULIP, taken an endowment plan, or believes that real estate "always" doubles.

Key Concepts and Frameworks

The 3-Account System. Income (salary lands here), Spend-It (the only one with a debit card), Invest-It (auto-debited on the 5th). Removes willpower from saving — and it has changed more Indian household finances than any financial product ever launched.

Emergency Fund = 6 months of essential expenses, parked in a liquid fund or sweep-in FD. Build this before you start equity investing.

Term insurance only, never bundled. A cover of 8–10 times annual income, or 15–20 times monthly expenses. Buy term, invest the difference.

Independent health insurance. A ₹5–10 lakh family floater, separate from your employer cover. Job loss is when you need it most.

Goal-bucketed investing. Almost-There goals (0–3 years) into debt. In-Some-Time goals (3–7 years) into hybrid. Far-Away goals (7+ years) into equity.

Demolishing the real estate and gold myths. Real estate's actual long-run return, after maintenance, taxes and registration, is closer to 8–10% than the lore suggests. Gold capped at 10% of portfolio — preferably via Sovereign Gold Bonds, which pay 2.5% additional annual interest.

Mutual funds over direct equity for most Indian households, with a clear preference for direct plans, low-cost index funds, and a small actively-managed core.

Famous Principles

"Insurance is not investment. Investment is not insurance."

— Monika Halan

"Each financial product you buy must solve a financial problem you have."

— Monika Halan

Indian Context Application

This is the most India-specific book on this list. EPF, PPF, NPS, ULIPs, ELSS, Section 80C, the new tax regime, mediclaim and motor insurance — it is all here, in plain language. The system Halan lays out is exactly what a fee-only SEBI Registered Investment Adviser would design for a household, except those advisers charge ₹25,000–₹50,000 a year and Halan charges you the price of a meal.

Criticisms

If you are looking for direct-equity stock-picking, this is the wrong book — deliberately so. Halan's worldview is that most Indians should not pick stocks and should focus on a low-friction, low-error, automated system. Some advanced investors find it too conservative. They are missing the point: this book is the foundation under everything else.

One-line takeaway: Set up the 3-account system this weekend, buy term and health insurance this month, and begin your SIPs from the next salary cycle.

#3. Coffee Can Investing — Saurabh Mukherjea

Coffee Can Investing: The Low-Risk Road to Stupendous Wealth

Authors: Saurabh Mukherjea, Rakshit Ranjan, Pranab Uniyal | Published: 2018 | Publisher: Penguin Portfolio

Pages- 240

Reading Time~6 hours

Price (India)- ₹250 – ₹400

Best For - Intermediate equity investors

Difficulty - Moderate

Languages - English, regional editions

By the time you reach Mukherjea, you have the mindset (Housel) and the system (Halan). Now you want to build a direct-equity satellite portfolio without losing money. This is the book for that.

Mukherjea — formerly CEO of Ambit Capital and now the founder of Marcellus Investment Managers — adapts a 1984 American concept by Robert G. Kirby for Indian markets. The idea: build a portfolio of 10–25 high-quality companies and leave it untouched for a decade. The Coffee Can rewards laziness.

Key Concepts and Frameworks

The Twin Filters. Pick Indian companies that have delivered (1) revenue growth of at least 10% every single year for 10 consecutive years and (2) Return on Capital Employed (ROCE) of at least 15% every single year for 10 years. For banks, replace the second filter with a loan-book growth of 15%.

Minimum market cap ₹100 crore to ensure liquidity.

Hold for 10 years. No churning, no panic selling, no rebalancing.

The compounding math. At 26% CAGR, ₹1 becomes ₹10 in 10 years and ₹100 in 20 years. At 20% CAGR, it still becomes ₹38 in 20 years.

B2C bias. Consumer brands, retail banks, and pharma dominate ideal CCP picks because of repeat purchase, brand moat, and pricing power.

Mutual fund cost critique. Expense ratios silently destroy long-run returns. Use direct plans + index funds for the bulk of your portfolio.

Indian Case Studies

The book is wall-to-wall Indian companies you can buy today: Asian Paints, HDFC Bank, Page Industries, Marico, Pidilite, Berger Paints, Nestlé India, Titan, HUL. The "consistent compounders" thesis it lays out is the same one that anchors Marcellus's flagship PMS strategies — which themselves have become benchmarks for Indian quality investing.

Famous Principles

"The Coffee Can Portfolio rewards the lazy investor — but only the lazy investor who picked the right cans."

— Saurabh Mukherjea

Indian Context Application

You can implement this book the same day you finish reading it. Open Screener.in, plug in the ROCE ≥15% and revenue-growth ≥10% filter for the last 10 years, screen out micro-caps under ₹100 crore, and you will land with a manageable shortlist. Pick 12–15 names, allocate equally, and lock the portfolio.

Criticisms

Critics on Goodreads have pointed out that some of the book's back-tested 20–26% CAGR figures look aggressive, and the 80% equity suggestion for near-retirees is debatable. Coffee Can performance since 2018 has been mixed during the 2022–23 mid-cap correction, and Marcellus's own funds have had stretches of underperformance. Read this book alongside The Intelligent Investor (next on the list) so you are not seduced by single-style optimism.

One-line takeaway: Screen for ROCE ≥15% and revenue growth ≥10% over 10 years, pick 12–15 stocks, buy equal-weight, and lock the portfolio for a decade.

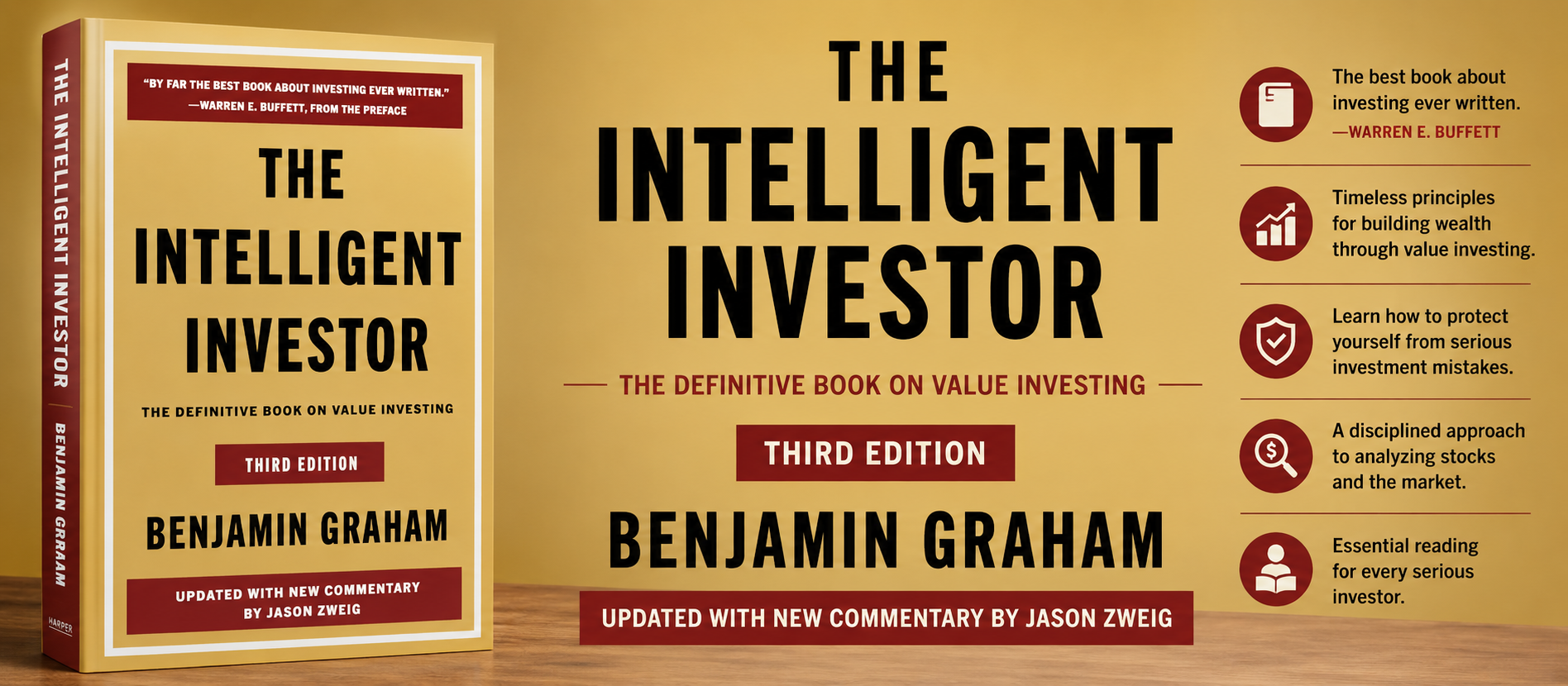

#4. The Intelligent Investor — Benjamin Graham

The Intelligent Investor

Author: Benjamin Graham | First Published: 1949 (Revised edition with Jason Zweig commentary, 2003) | Publisher: HarperCollins

Pages~640

Reading Time~20 hours

Price (India) - ₹400 – ₹700

Best For - Intermediate to advanced

Difficulty- Challenging

Languages - English, Hindi, regional

Warren Buffett calls this "by far the best book on investing ever written." That should be enough. But here is the question every Indian reader asks: why should I read a 1949 book about American railroads in 2026?

Because Mr. Market is the same animal in Mumbai as he is in Manhattan. Graham's two big ideas — Mr. Market and Margin of Safety — are the bedrock under every successful Indian fund manager from Rakesh Jhunjhunwala to Prashant Jain to Saurabh Mukherjea himself.

Key Concepts and Frameworks

Investment versus speculation. Graham's most quoted definition: "An investment operation is one which, upon thorough analysis, promises safety of principal and an adequate return. Operations not meeting these requirements are speculative." If you cannot define the difference, you are speculating.

Defensive vs. Enterprising investor. Pick one. The defensive investor wants a simple, low-effort, mostly indexed portfolio. The enterprising investor is willing to do the work to beat the market. Most Indian retail investors think they are enterprising; they are actually defensive who chose the wrong category.

Mr. Market (Chapter 8). Buffett calls this chapter the single most important essay ever written on investing. Imagine the market as a bipolar business partner who shows up every day offering to buy your shares or sell you his — at wildly different prices. You are free to accept his offer, refuse it, or simply not answer the door.

Margin of Safety (Chapter 20). The central concept of the entire book. Never buy without a cushion against your own analytical error. If your estimate of fair value is ₹100, refuse to pay more than ₹70.

Quantitative screens for the defensive investor. P/E under 15, P/B under 1.5, current ratio over 2, positive earnings for 10 consecutive years, dividend record for 20.

The Graham Number. Square root of (22.5 × Earnings Per Share × Book Value Per Share). A rough intrinsic-value yardstick.

Dollar-cost averaging. The intellectual ancestor of the Indian SIP.

Famous Quotes

"In the short run, the market is a voting machine, but in the long run, it is a weighing machine."

— Benjamin Graham

"The intelligent investor is a realist who sells to optimists and buys from pessimists."

— Benjamin Graham

Indian Context Application

The case studies (American railroads and 1950s utilities) feel dated. The principles do not. Use the 2003 Jason Zweig revised edition — Zweig's running commentary bridges Graham's 1940s text to modern markets, including the dot-com bust. Apply Graham's screens to Indian companies through Screener.in or Tijori. Most importantly, internalise the Mr. Market parable. The next time Bank Nifty is down 5% and CNBC anchors are panicking, you will smile and add to your SIP.

Criticisms

It is genuinely difficult. Many Indian readers take 6–18 months to finish it. The prose is dense, the examples are old, and some chapters read like a history lesson. If you are struggling, read just Chapters 1, 8 and 20. Those three chapters alone are worth the price.

One-line takeaway: Before buying any stock, write down your estimated intrinsic value and refuse to pay more than 70% of it.

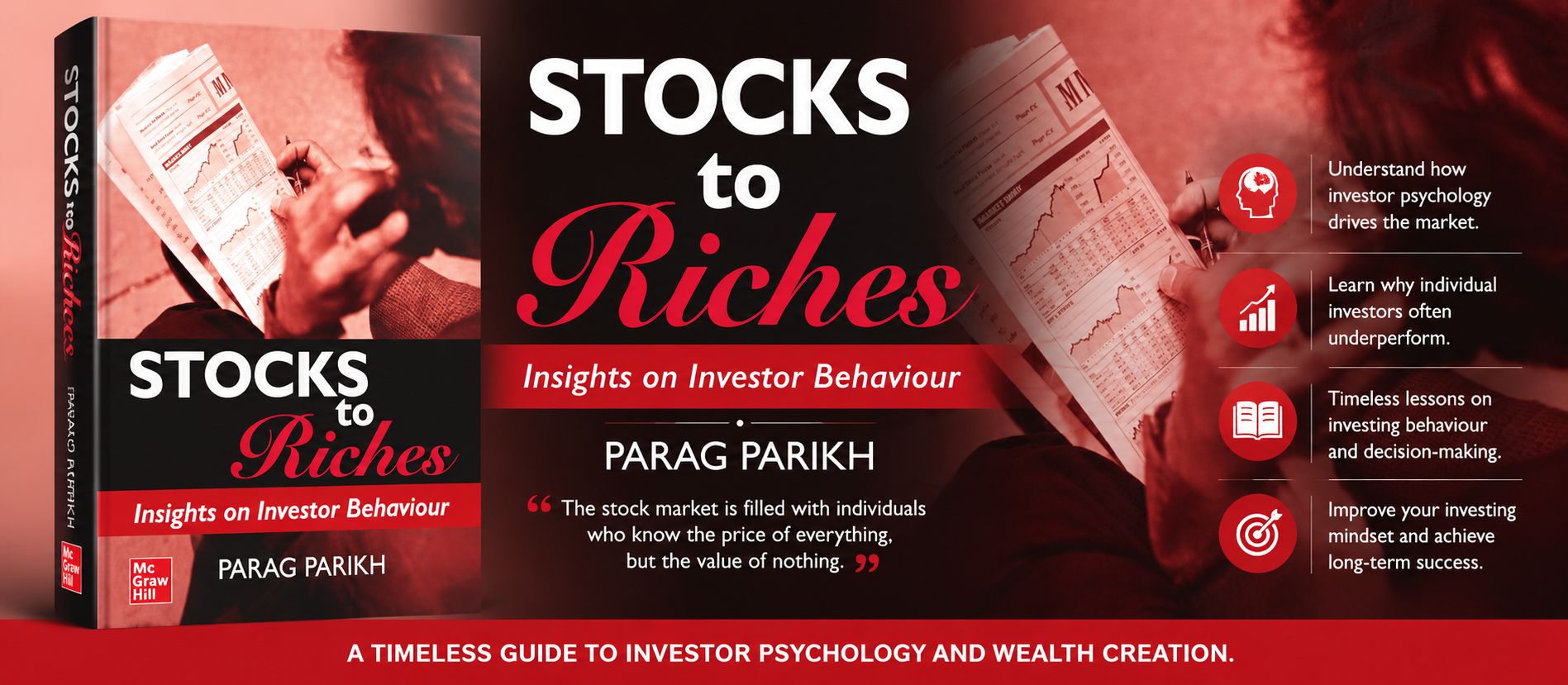

#5. Stocks to Riches — Parag Parikh

Stocks to Riches: Insights on Investor Behaviour

Author: Parag Parikh | Published: 2005 | Publisher: Tata McGraw Hill

Pages~200

Reading Time~5 hours

Price (India) - ₹200 – ₹350

Best For - Indian equity beginners

Difficulty - Easy to moderate

Languages - English

The fifth and final book on this list is, paradoxically, the oldest of the Indian-authored ones. The late Parag Parikh — founder of PPFAS Mutual Fund, whose Parag Parikh Flexi Cap Fund is today one of India's largest actively managed equity schemes — was the first Indian to popularise behavioural finance for Indian retail investors.

This is a slim, fast-reading book that punches far above its weight. It is the closest you can get to a "Indian Daniel Kahneman" — Parikh takes the principles of behavioural finance and translates them into Indian stock market disasters you already remember.

Key Concepts and Frameworks

Investment vs. speculation vs. gambling. Parikh draws a sharp line that most Indian "investors" never see. The 91% F&O loss-makers, the IPO-listing-day flippers, the small-cap chasers — all are speculators or gamblers, not investors.

Behavioural biases in Indian dress. Herd mentality (the IT bubble of 2000, the small-cap mania of 2017, the SME-IPO frenzy of 2024), loss aversion, anchoring, mental accounting (Richard Thaler), endowment effect, status-quo bias — every chapter is an Indian case study.

Heuristic traps. Representativeness ("this stock looks like Infosys in 1995, so it will become the next Infosys"), availability ("I just read about EV stocks, so they must be the future"), hindsight bias ("I knew Yes Bank would crash all along").

Indian market history dissected. The Harshad Mehta scam, the Ketan Parekh bubble, and the dot-com bust — used not for nostalgia but for behavioural diagnosis.

Why most mutual funds underperform. Incentive misalignment, asset-gathering instead of asset-management, and the perils of style drift.

The Four E's for investing success. Earnings, Equity (ownership), Endurance (long-term), Emotions (control).

Famous Principles

"Investments do well, but investors don't."

— Parag Parikh

"The stock market is a wonderful mechanism for transferring wealth from the impatient to the patient."

— Parag Parikh

Indian Context Application

The most actionable behavioural-finance book for an Indian investor. After finishing it, write down the single bias you are most prone to — overconfidence? loss aversion? recency? herd? — and install a checklist that forces you to question that bias before every buy or sell decision. That one habit alone will outperform 90% of trading courses.

Criticisms

The book is short and at times reads like a curated survey of behavioural ideas rather than a deep dive. It is also light on "how to actually pick a stock" — pair it with Coffee Can Investing for that. The 2005 publication date means there are no examples from the 2008 crash, demonetisation, or COVID — but the principles need no update because human behaviour does not.

A Note on the Author

Parag Parikh tragically passed away in 2015 in a road accident in Omaha while attending the Berkshire Hathaway Annual General Meeting. PPFAS continues to follow his philosophy under his son Neil Parikh's leadership, but no new editions of the book are forthcoming. Treat it as a finished classic.

One-line takeaway: Identify your biggest behavioural bias and install a checklist that forces you to question it before every buy and sell.

Quick Comparison Snapshot

If you are short on time, here is the entire reading list in a single table. Use it to decide which book to pick up first based on your current stage as an investor.

# | Book | Author | Focus | Pages | Price (₹) | Best For |

|---|---|---|---|---|---|---|

1 | The Psychology of Money | Morgan Housel | Mindset & Behaviour | 256 | 250 – 350 | Everyone |

2 | Let's Talk Money | Monika Halan | Personal Finance System | 204 | 250 – 350 | Indian Salaried Beginners |

3 | Coffee Can Investing | Saurabh Mukherjea | India Equity Strategy | 240 | 250 – 400 | Intermediate Investors |

4 | The Intelligent Investor | Benjamin Graham | Value Investing Framework | ~640 | 400 – 700 | Advanced Readers |

5 | Stocks to Riches | Parag Parikh | Behavioural Finance | ~200 | 200 – 350 | Indian Equity Beginners |

Honourable Mentions: The Next 7 Books

If you finish all five and want more, here is your next shelf — also heavily weighted toward Indian context and Indian authors.

Rich Dad Poor Dad — Robert Kiyosaki (1997). Best for the assets-vs-liabilities mindset shift. Light on actionable detail, but a great motivational starter. ₹200–₹350.

One Up On Wall Street — Peter Lynch (1989). "Invest in what you know" — works beautifully in India where you can observe DMart, Zomato, Asian Paints in daily life. ₹300–₹500.

Common Stocks and Uncommon Profits — Philip Fisher (1958). The 15-point scuttlebutt method for evaluating Indian mid-caps with limited public information. ₹350–₹500.

Bulls, Bears and Other Beasts — Santosh Nair (2018). A narrative history of the Indian stock market from the 1990s scams to the modern era. ₹350–₹500.

The Dhandho Investor — Mohnish Pabrai (2007). Indian-American Buffett disciple; "heads I win, tails I don't lose much" framing applied to Indian-style asymmetric bets. ₹400–₹600.

The Unusual Billionaires — Saurabh Mukherjea (2016). Deeper case studies of seven Indian compounders. The natural companion to Coffee Can Investing. ₹350.

Let's Talk Mutual Funds — Monika Halan (2023). The fund-by-fund category guide that picks up where Let's Talk Money left off. ₹350.

Your 6-Month Reading Roadmap

Reading without sequence is reading without compounding. Here is the exact order, with implementation milestones for each month.

Month | Book | Implementation Goal |

|---|---|---|

Month 1 | The Psychology of Money | Open a Nifty 50 index-fund SIP for ₹5,000–₹10,000. Write down your 5 personal money beliefs. |

Month 2 | Let's Talk Money | Set up the 3-account system. Buy term insurance and ₹5–10 lakh health cover. Build a 6-month emergency fund. |

Month 3 | Stocks to Riches | Write down your top 3 behavioural biases. Create a pre-trade checklist that forces you to confront each one. |

Month 4–5 | Coffee Can Investing | Run the ROCE + revenue-growth screener on Screener.in. Identify 12–15 stocks. Begin a small "satellite" equity portfolio. |

Month 6 | The Intelligent Investor (Chapters 1, 8, 20) | Write your one-page Investment Policy Statement. Define your no-go zones (e.g., "no F&O ever"). |

Common Mistakes Indian Investors Make — and Which Book Fixes Them

Mistake | Book That Fixes It |

|---|---|

Treating F&O / intraday as "investing" (91% lose) | Stocks to Riches; The Intelligent Investor |

Stopping SIPs in market downturns (39 lakh stopped in Nov 2024) | Psychology of Money; Let's Talk Money |

Bundling insurance with investment (ULIPs, endowment) | Let's Talk Money |

Chasing thematic NFOs and IPOs | Coffee Can Investing; The Intelligent Investor |

Following unregistered finfluencers on Telegram and YouTube | Stocks to Riches; Psychology of Money |

Over-allocating to gold and real estate, under-allocating to equity | Let's Talk Money; Coffee Can Investing |

Frequent portfolio churn that destroys compounding | Coffee Can Investing |

Confusing high income with real wealth | Psychology of Money |

Overconfidence after a few lucky trades | Stocks to Riches; Intelligent Investor |

Starting equity investing before having insurance or emergency fund | Let's Talk Money |

Best Practices for Reading Investment Books

Owning a stack of investing books is not the same as becoming a better investor. Here is how the most disciplined Indian wealth builders actually use them.

Read in sequence, not in parallel. Investing books reward depth. Read one, implement its lessons, then move on.

Maintain a one-page "Lessons" note per book. Five rules per book, no more. Written in your own words, not highlighted from the text.

Write a personal Investment Policy Statement. After each book, refine it. Include asset allocation, monthly SIP amount, rebalancing rules, no-go zones.

Implement before you finish. By the time you close Let's Talk Money, your 3-account system should already be live.

Track behaviour, not just returns. Maintain a trade journal with the reason for every buy and sell. Most retail investors quit speculation once they confront their own data.

Re-read the best two every 2–3 years. Psychology of Money and Stocks to Riches hit very differently after living through one full market cycle.

Discuss the books. Join a book club, talk to a SEBI-Registered Investment Adviser, or share notes with a friend who is also serious about wealth building.

Expert Insights: What India's Top Voices Say

The 2025–26 Indian Investing Trends to Know

Behavioural finance is going mainstream. Psychology of Money has been on Amazon India's top-10 finance bestseller list almost every week since 2021.

Passive investing is booming. India's passive MF AUM has grown from ~₹14,000 crore in March 2015 to about ₹13 lakh crore by October 2025 — roughly 16.7% of total MF AUM.

FIRE in India is more conservative than global FIRE. Indian FIRE practitioners typically use a 3–3.5% safe withdrawal rate (vs. the global 4%) due to longer life expectancy and higher inflation.

India-first books are taking over. Mukherjea, Halan, Parikh, Pranjal Kamra and Santosh Nair now sit on bestseller lists alongside Graham, Lynch and Housel.

Vernacular finance reading is rising. Hindi, Marathi, Tamil, Bengali and Punjabi editions of major investment books are growing rapidly.

The CFA Institute's March 2025 report titled "Clicks and Credibility" found that only about 2% of finfluencers are SEBI-registered, yet 33% provide explicit stock recommendations, and 63% fail to adequately disclose sponsorships or financial affiliations. In a country where short-form video is replacing books for a generation, the case for sitting down with a 250-page paperback by a credentialed author has never been stronger.

Final Thoughts

Wealth in India in 2026 will not be built by the cleverest trader, the most plugged-in finfluencer follower, or the smartest IPO flipper. It will be built by the patient SIP investor who read five books, wrote a one-page Investment Policy Statement, and then simply stopped checking the market.

Of all the products being sold to Indian retail investors today — F&O courses for ₹15,000, "advisory services" for ₹25,000 a year, premium Telegram channels for ₹5,000 a month — the five paperbacks on this list are the only ones with a guaranteed positive return.

The total cost is under ₹2,000. The total reading time is about 40 hours. The total impact, over a 30-year compounding horizon, can be the difference between a comfortable retirement and a confused one.

Start tonight with The Psychology of Money. Or better — buy all five today, line them up on a shelf you can see, and read one a month for the next five months. By the time you close the last page of the last book, you will be a different kind of investor. And the markets, finally, will be your ally instead of your adversary.

Frequently Asked Questions

0 comments